Nonresidential CRE Loans Are Leaving Skid Marks on Banks

[ad_1]

Thankfully, they’re only a small-ish part of the banking industry’s overall loan book. But some banks are more exposed than others.

By Wolf Richter for WOLF STREET.

Banks are still very profitable. The industry reported quarterly net income of $64 billion in Q1, according to the FDIC yesterday. And so overall, as an industry, they can take big credit losses, and they have started to take growing credit losses. But some banks are more exposed to risks and are more fragile than others.

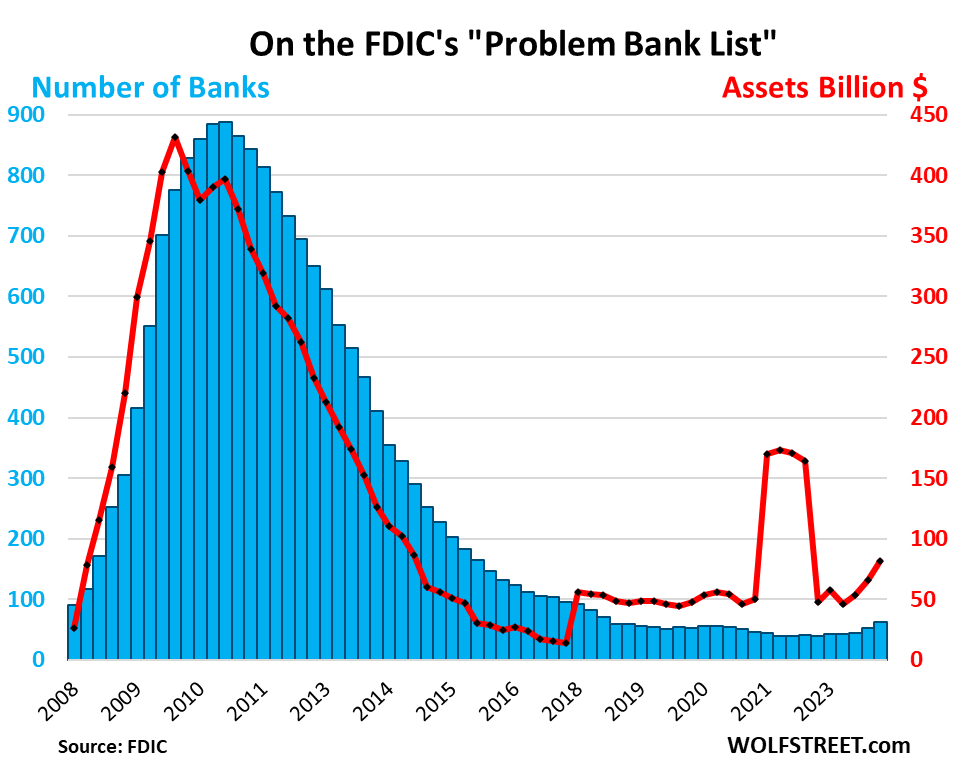

Banks on the FDIC’s “Problem Bank List” rose by 11 banks in Q1 from the prior quarter, to 63 banks (blue columns), of the 4,000-plus banks in the US. The FDIC doesn’t name names, but we can guess some candidates. So there will be some more bank failures – there are nearly always every year.

Total assets on the Problem Bank List rose by $16 billion in Q1, to $82 billion, the third consecutive quarter of deterioration (red line), largely driven by the quagmire that CRE has been sinking into. The chart shows the historic context to the Financial Crisis:

CRE is starting to leave skid marks.

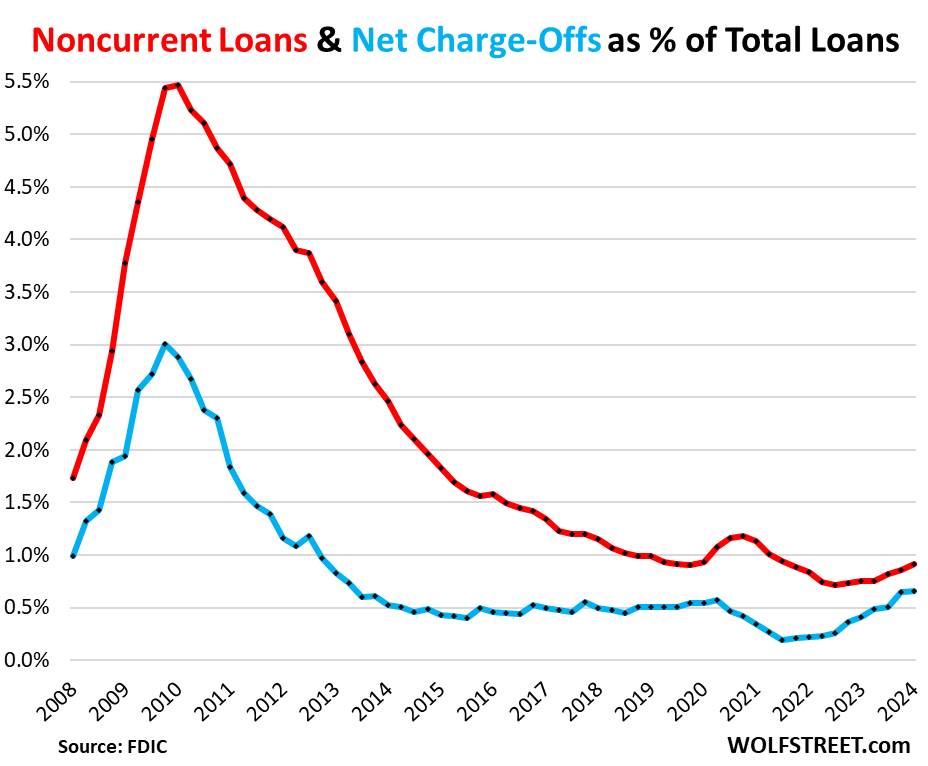

Noncurrent loans (where borrowers fell behind) rose to 0.91% of total loans (from 0.86% in the prior quarter), now roughly at the same rate as during the Good Times just before the pandemic. At the peak during the Financial Crisis, it had hit 5.5% (red).

The deterioration was driven by CRE loans, where the noncurrent rate rose to 1.59%, the highest since Q4 2013, driven by office portfolios at the largest banks.

Net charge-offs (when banks throw in the towel on the loan) were 0.65% of total loans, same as in the prior quarter, but up from the historic free-money-from-heaven pandemic era lows, and a hair higher than during the Good Times before the pandemic. The driver behind the increase from the free-money lows in 2022 were credit cards, where the net charge-off rate rose to 4.70% in Q1, up by 122 basis points from its pre-pandemic average. We went into the weeds of who was falling behind on their credit cards here.

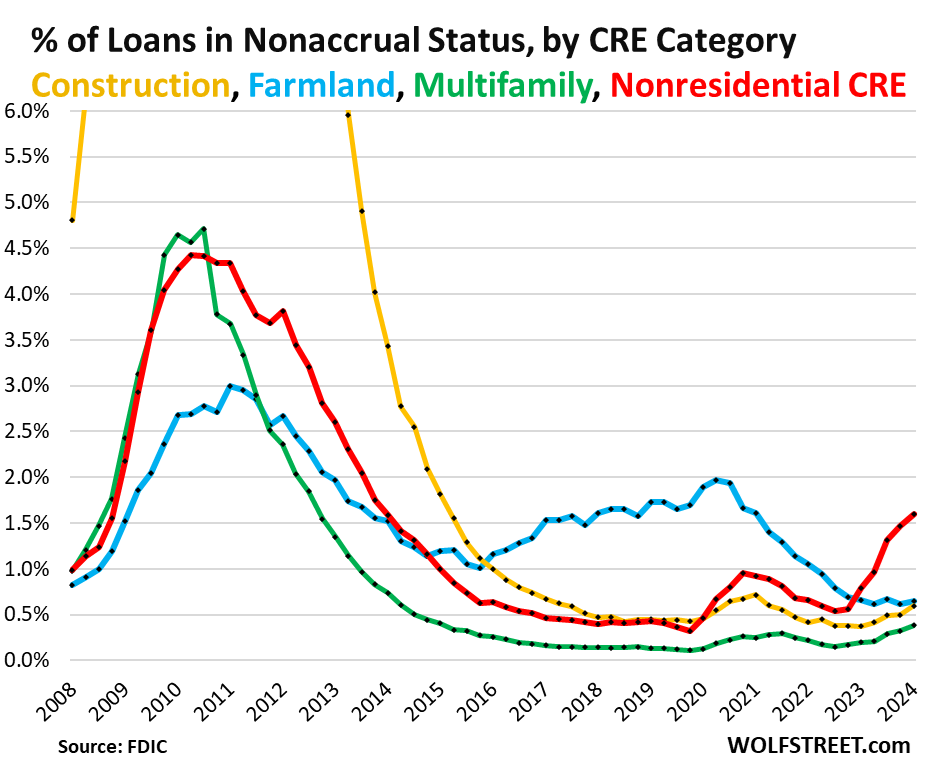

Nonaccrual rates by CRE category.

The chart below shows how nonresidential nonfarm CRE loans (red) have become the outlier in terms of nonaccrual rates, compared to other CRE categories, such as construction loans (yellow), farmland loans (blue), and loans on multifamily buildings (green).

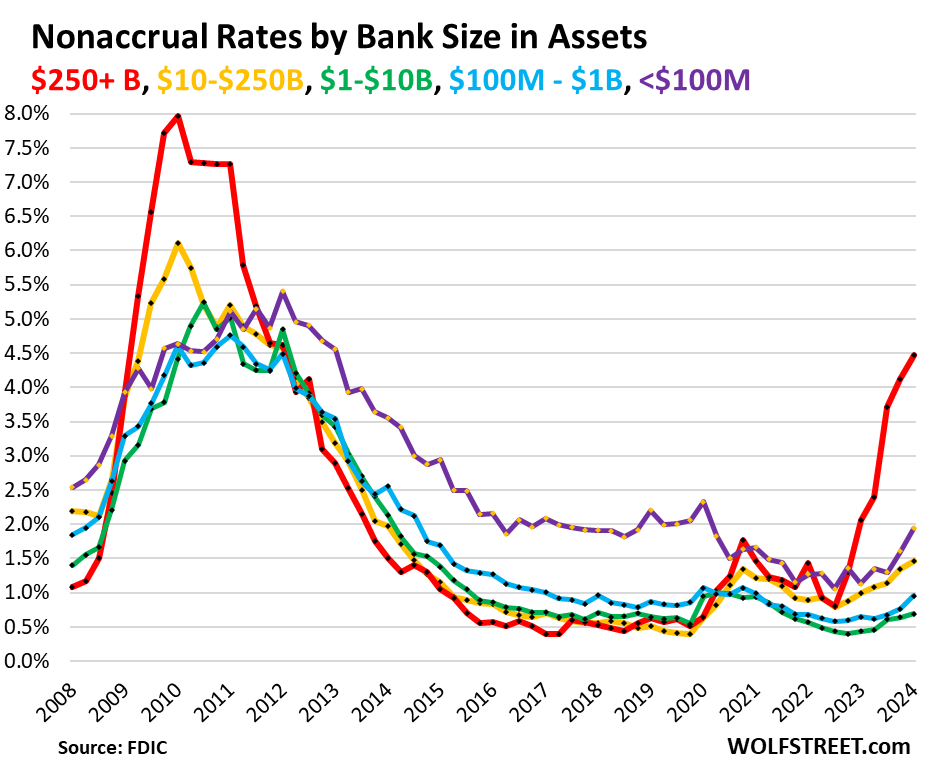

Nonresidential CRE loans at big banks get messy.

FDIC provides delinquency data by bank size on nonresidential nonfarm CRE loans (which include the most troubled sectors of CRE lending, office and retail). The “past-due and nonaccrual rates” of these CRE loans have increased across all bank sizes.

But for large banks with over $250 billion in assets, the rate for nonresidential CRE loans spiked to 4.48% of total loans (red in the chart below).

During the Financial Crisis, the big culprit were residential mortgages, a much larger category of loans than nonresidential CRE loans. At this point, residential mortgages are still in good shape with historically low delinquency rates and foreclosures.

For tiny banks with less than $100 million in assets, the “past-due and nonaccrual rate” jumped to 1.94% (purple).

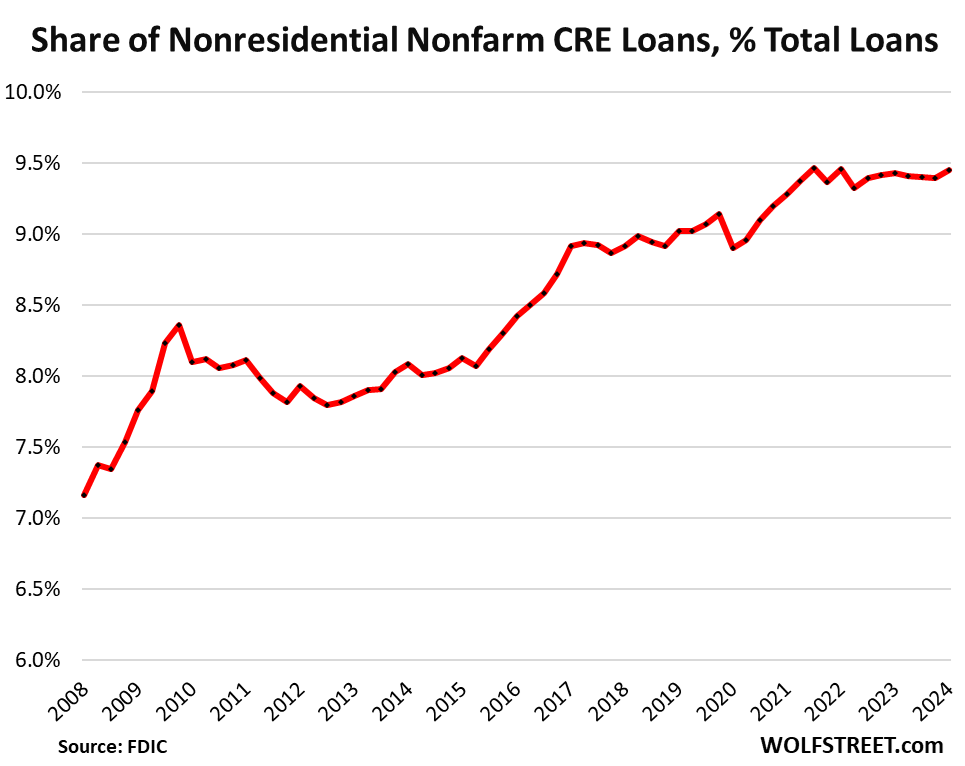

Thankfully…

Nonfarm nonresidential CRE loans – where the bulk of the loan problems are now occurring – form only a small part of the banks’ total loan book. In Q1, these loans amounted to 9.4% of total bank loans. Since 2021, the share has been roughly in the same range, just under 9.5%. And the fact that the share of the loan book overall isn’t bigger is a good thing, given how problematic these CRE loans are going to be as the sector cleans house, so to speak, over the next few years:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

[ad_2]

Read Nore:Nonresidential CRE Loans Are Leaving Skid Marks on Banks

Comments are closed.